The universal performance curve - or how to invest properly in a classic

10/09/2014

Predicting the value of a car is bordering on magic. Hardly anyone would have expected 40 or 45 years ago that the unhelpful Ferrari 250 GTO, which could be bought for 20,000 francs (or 24,000 DM) at the time, would one day change hands for a hundred times that value.

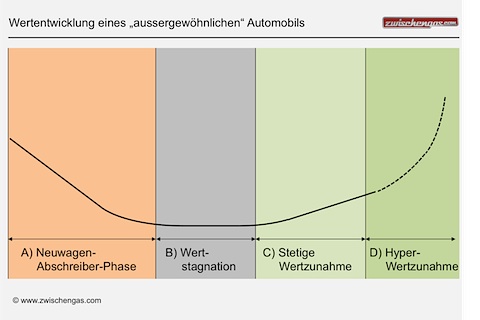

Nevertheless, the value of most cars follows a similar curve over and over again: first, the newly purchased car loses value continuously and massively, depending on the type of vehicle and its state of preservation, the loss in value is 15 to 30% per year (in exceptional cases less or more), until after a few years, after a slowdown in the decline in value, a ceiling is reached. This is the end of phase A and we then usually move on to phase B, during which the car's value remains constant until it slowly but steadily increases in value in the transition to phase C. This phase C can last a long time and the value of the vehicle usually only increases slightly each year, making up for the loss of purchasing power of the money, so to speak.

For very special automobiles, the value of the car then increases disproportionately in a fourth phase D. Even hyper-value increases are then possible, depending on the preferences of the collectors at that time and, of course, depending on the attractiveness of the vehicle type in the context of the production quantity and usability of the vehicle.

For most cars, however, continuous value growth ("D2") simply continues in the fourth phase, perhaps somewhat accelerated, but relatively straightforward. And in some cases, the growth may level out ("D3") or even enter a further phase of depreciation because the interests of classic car buyers have changed or the state exerts influence by changing regulations.

The wise investor is best advised to buy at the end of the stagnation phase, provided he has enough time, because this way he can capture the full potential increase in value.

Investors who focus on short-term gains, however, look for the vehicles that are just before the "D" phase and can double their money in a short time. We can currently see that this is happening in the price increases for Porsche 911 Carrera RS, Lamborghini Miura (and early Countach) or sought-after Ferrari models. The problem is that these increases in value are a consequence of market forces and not necessarily of attractiveness from the collector's point of view. It is therefore also unclear how sustainable these increases in value really are.

For the majority of classic car enthusiasts, this does not matter anyway, because they are sitting in a classic car that is increasing in value along curve "D2" (above), albeit more slowly but steadily.

For youngtimer buyers, it should also be added that most of the more attractive youngtimers are typically at the end of phase B and further losses in value can therefore usually be ruled out. However, as discussed earlier, it is questionable whether the increase in value compensates for maintenance and upkeep costs.

And one more note: If purchasing power, currency fluctuations and inflation are taken into account in these considerations, then the shape of the curve is not necessarily influenced in the long term, but its characteristics certainly are.